Links

Government Intervention

By Kate Lawrence

The classic, and contentious, Keynesian argument—whether or not intervention of government policies (and funds) aids in the security and success of markets—seems increasingly mute these days, as the international economic recession has motivated governments to pledge aid, fund stimulus packages, and rethink financial and tax programs for businesses across the board.

In the realm of shipping, the simultaneous economic and credit crises have had significant impact on the ability of certain registers to maintain their viability, calling in to question critical government policy changes as they pertain to industries with strong offshore and overseas bases.

The European Commission’s 2009-2010 Maritime Transport Strategy Communication has stressed the importance of pursuing appropriate government action to ensure the continuous performance of the E.U. maritime transport industry. This includes government support of European registers, which face increasing competition from ‘third country’ companies, which enjoy more the considerable financial and legal backing of their own governments.

Battling on All Fronts

We don’t envy Geoff Jones, the CFO of Trico Marine Services (“TMS”), and the rest of the team at Trico, who have been very busy of late. In just the last two weeks, they have worked to bring order to their balance sheet by reducing debt and increasing liquidity. The first step in the process was the sale of two North Sea supply vessels in line with the company’s strategy to reduce both spot OSV exposure and its dependence on the supply vessel market. The proceeds of approximately $40 million will be used to repay outstanding European bank debt.

The company also reached an agreement with the shipyard in India that was constructing the seven remaining subsea service vessels. The first three will be delivered as scheduled between December 2009 and July 2010. Trico received price concessions on these three vessels, which will require only an additional $40 million to complete. Delivery of the last four subsea service veesels has been suspended with the company retaining the right to cancel its obligation to take delivery of these vessels. By preserving the option to construct these vessels, the company retains the flexibility to develop its strategic growth plans for subsea services in accordance with market conditions and liquidity requirements at a future date. The net effect of this suspension is to reduce committed capital expenditures for 2010 and 2011 by $80 million.

Waived

After a rather quiescent period, last week marked the return of waivers and restructurings. Seanergy Maritime Holdings announced that it 50% owned affiliate, Bulk Energy Transport (Holdings) Limited had signed a supplemental agreement with its lenders receiving a reduction of the security requirement and minimum equity ratio for the period up to July 1, 2010.

DryShips also announced that it had finalized its previously agreed waivers with the German banks, Nord LB and West LB covering their respective loans of $116 million and $67 million. According to Mr. Economou, “We are now left with $187.5 million of outstanding debt, where constructive discussions with the banks continue for waivers and we expect to have those concluded shortly.” What a long hard road it’s been.

“BDI” and We Don’t Mean the Index

Leave it to Peter G. Current thinking suggests that the investing world is trading dry shares as a proxy for the BDI. So what does Peter G do? Through his dry bulk operating company, Genco Shipping and Trading (“Genco”) he forms a new subsidiary called interestingly enough, Baltic Trading Limited (“Baltic”) The goal of the new venture is to provide shareholders with the opportunity to invest in a company with a strategic focus on the drybulk spot market, which utilizes little to no leverage and seeks to distribute regular dividends based upon earnings. This, of course, is in contrast to its parent, which is more time chartered focused.

Genco then announced on Wednesday that the new company, to be led by John Wobensmith, had filed a registration for a proposed initial public offering of common shares (Class A shares). With only a red herring filed at the time of writing, details are scant, however the registration document indicates a maximum offering of $230 million. The book runners are Morgan Stanley and Dahlman Rose.

Continue Reading

The China Story Continues

Trying to get a sense of how huge the ship finance market in China has always been a daunting challenge for us. The domestic banks are highly competitive and remain guarded when it comes to disclosing their ship finance transactions. In our quest to make the market more transparent, we are very pleased to make some progress. This year, for the very first time in history, Industrial and Commercial Bank of China (“ICBC”) shared with us the size of their shipping portfolio in our annual bank debt survey. And likewise, for the very first time in Singapore, we are very grateful to Ms Helen Zeng, Senior Relationship Manager from Bank of China (“BOC”) for taking time off her busy work schedule in Beijing to share with us her views on the Chinese market at our conference. Continue Reading

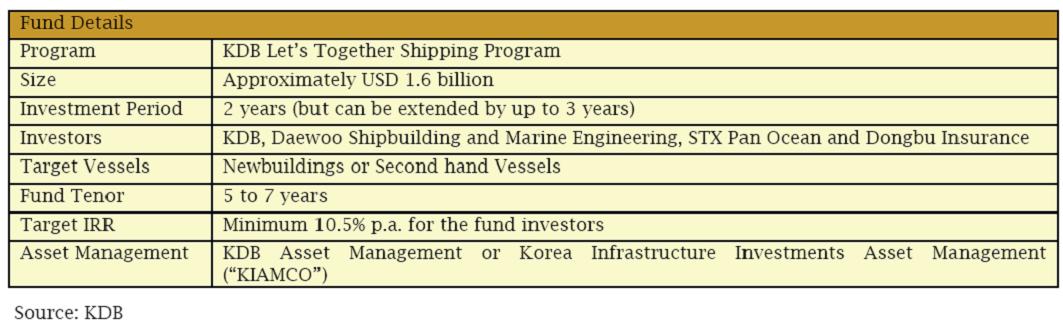

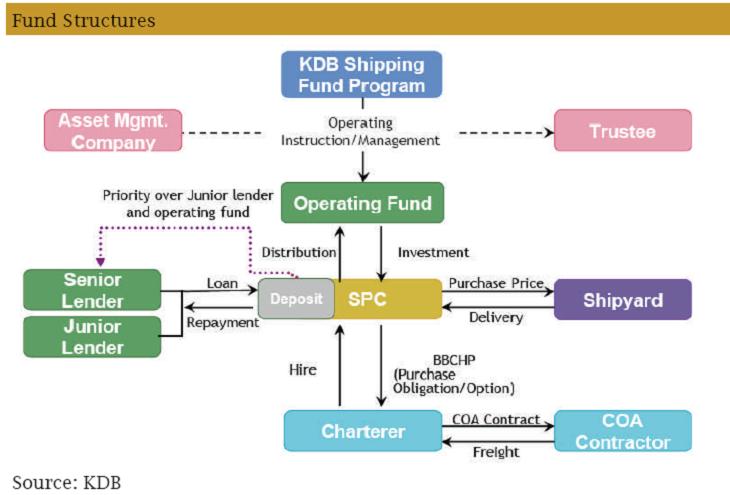

Let Us Get Together

The Korean shipping finance market remains challenging but it is heartening to note one Korean financial institution is thinking out of the box and supporting its core clients. On the second day of Marine Money Asia Week, we had the pleasure to listen to Mr. Dong Hae Lee, Head of Shipping Finance Team at the Korea Development Bank (“KDB”). Mr. Lee told the audience that Korean shipping companies continue to suffer losses from operations which have led to several cases of corporate restructuring and liquidation in the country. But the good news is there are several avenues for Korean owners and operators to strengthen their balance sheets now.

For the big boys, self help is important. Korea Line, Hanjin Shipping, STX Pan Ocean, Hyundai Merchant Marine, SK Shipping and Eukor Car Carriers have raised over KRW 2.93 trillion (USD 2.5 billion) from the domestic capital markets. And if the shipping company has secured Contracts of Affreightment (“COA”) earnings from the big freighters such as POSCO, KOGAS and KEPCO, asset-backed securitization and asset-backed loans can be arranged by the banks to enhance the operator’s liquidity position. In terms of sale and leaseback structures, both KDB and Korea Asset Management Corp (“KAMCO”) have introduced shipping funds to provide further financial support to the shipping industry. Continue Reading

Full House in Athens

Despite the tough market and the general lack of ship finance, Marine Money’s 11th Greek Ship Finance conference again filled the seats in Athens. With in excess of 300 delegates and speakers and some 40 more for the TEN Ltd lunch there was plenty gossip and exchange of views. Next week we will provide a full report of the conference.

Public or Private?

The question of whether to go public or stay private will never be satisfactorily answered, but it does make for good conversation. We had such a discussion with an owner recently who had some very interesting perspectives.

Not having to account for his actions to third parties, the traditional private owner can buy at the bottom of the cycle. So long as he has the necessary capital and liquidity to fund the investment, the vessel can, in the worst case, be laid up. This is not the case for a public owner who must enter into an accretive transaction. To accomplish this, he must buy along the bottom of the “U” shaped curve and have fixed employment that will provide sufficient cash flow to meet operating expenses, debt service, pay down the vessel to a reasonably attractive residual and finally provide a return. In short, the public buyer may pay more for a ship, give up the upside through the fixed rate charter and face residual risk at the end of the charter. His best outcome is a favorable average fleet cost.

The Invisible Hand

Adam Smith, in his classic work, The Wealth of Nations, posited the economic principal that the greatest benefit to society is brought about by individuals acting freely in a competitive marketplace in the pursuit of their own self-interest.

“It is not from the benevolence of the butcher, the brewer or the baker that we expect our dinner, but from their regard to their own self-interest… [Every individual] intends only his own security, only his own gain. And he is in this led by an invisible hand to promote an end which was no part of his intention. By pursuing his own interest, he frequently promotes that of society more effectually than when he really intends to promote it.”

While we are not sure whether Mr. Smith experienced a simultaneous economic and credit crisis in his time, we do know that today, as a result of these crises, it is not only individuals acting in their own self-interest. Banks, corporations and even governments are acting in the same manner. This should prove to be an interesting test of his thesis.

Managing Residual

The key to leasing both in terms of risk and profitability revolves around the management of residual. Cypress Leasing, an equipment lessor, today provided an example of just how it is done. Having three 22,351 DWT sister vessels, the Cape York, Cape Preston and Cape Conway redelivered by Schoeller Holdings upon the completion of a long-tern bareboat, the company entered into an agreement with G. Bros. Maritime to commercially and technically manage these vessels.

Although somewhat long in tooth, these general cargo vessels, built in 1983 and 1985, are a rare breed, which serve less developed areas in liner type services. Although their value is certainly depressed these days, these are solid Japanese built vessels, which we presume passed the 5th special survey prior to redelivery and were well taken care of by one of the top ship managers in the world. Given the long-term bareboat arrangement, we also assume that the vessels were written down to a conservative scrap level (say $150 to $200) allowing Cypress, with the downside covered (scrap today is > $300), to trade the vessels in the market and see if it can manage to make more money if the market turns in the next few years. The cost of this trade is minimal with the G. Bros. earning management fees and sharing in the profit.

The Official Guide To Marine Finance Providers

Shipping Index

{kind=link}

{kind=link}